Most homeowners do not think much about the difference between a home warranty and home insurance until something breaks, leaks, burns, stops working, or gets damaged.

Written by Tony Babarino, Luxury Real Estate Broker and REALTOR® with REAL Broker, serving Irvine, Newport Beach, Newport Coast, and Orange County, CA. DRE#01717758.

That is when the question becomes practical:

Who do I call, and what might actually be covered?

A home warranty, also called a home protection contract in California, is usually a service contract that may help with certain covered repairs or replacements when specific home systems or appliances fail from normal wear and tear. The California Department of Insurance describes a home warranty as a contract between a home protection company and a homeowner for repairing or replacing parts of a home system or certain appliances.

Home insurance, often called homeowners insurance, is different. It may help protect the home, personal property, and liability when a covered event causes damage or loss.

For homeowners in Irvine, Newport Beach, Newport Coast, South Orange County, and nearby coastal Orange County, this difference can matter before something goes wrong and before a home ever goes on the market. Buyers often notice condition, maintenance, signs of repairs, roof age, HVAC age, and whether the home feels well cared for.

The simple answer is this:

Home insurance is generally for covered sudden losses. A home warranty is generally for certain covered breakdowns.

The details, though, depend on the actual policy, contract, company, cause of the problem, exclusions, deductibles, service fees, limits, and claim decision.

Key Takeaways

- Home insurance and a home warranty are not the same thing.

- Homeowners insurance may help with covered property losses, personal belongings, liability, and certain sudden damage events, depending on the policy.

- A home warranty may help with certain covered home system or appliance breakdowns caused by normal wear and tear, depending on the contract.

- A home warranty does not replace homeowners insurance.

- If you are preparing to sell a home in Irvine, Newport Beach, Newport Coast, or coastal Orange County, understanding both can help you answer buyer questions with more confidence.

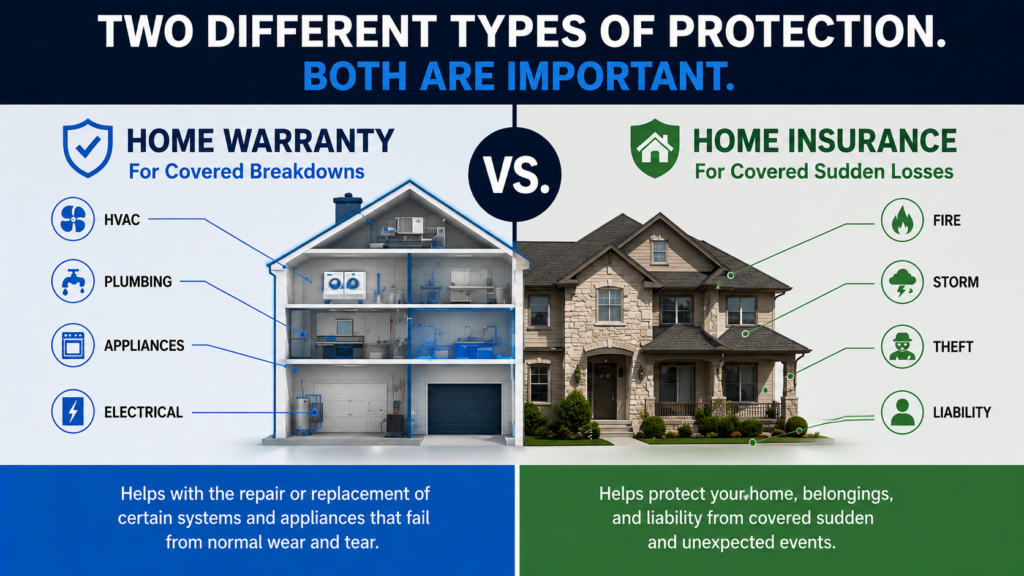

Warranty vs. Insurance: The Simple Difference

Here is the easiest way to think about it:

Home insurance is usually for covered sudden losses.

A home warranty is usually for certain covered breakdowns.

For example, if a windstorm damages part of your roof, that is generally the type of situation where a homeowner may review their homeowners insurance policy.

If your dishwasher stops working because a covered part failed from normal use, that may be the type of situation where a homeowner may review the home warranty contract.

The mistake is expecting one type of protection to do the job of the other.

What Is Home Insurance?

Home insurance is designed to help protect your home and belongings from certain covered events, subject to the policy terms.

Depending on the policy, homeowners insurance may include coverage for:

- The structure of the home

- Personal belongings

- Other structures on the property

- Loss of use or additional living expenses

- Personal liability

- Medical payments to others

Common covered events may include things like fire, theft, wind, or certain types of sudden water damage. But homeowners should not assume every situation is covered.

Standard homeowners insurance usually does not cover every possible risk. Earthquake and flood coverage, for example, are often separate or may require additional coverage. The National Association of Insurance Commissioners notes that earthquake damage is not usually covered by a standard homeowners or renters policy, and flood coverage is typically handled separately.

For California homeowners, this is especially important because insurance has become a much bigger topic in recent years. Wildfire risk, roof condition, replacement cost, brush clearance, and availability of coverage can all matter.

Your homeowners insurance policy is a legal contract. It is worth reviewing it with your licensed insurance professional so you understand what is covered, what is excluded, what your deductible is, and whether your coverage still fits your home.

Is Home Insurance Required?

California does not generally require homeowners to carry homeowners insurance. However, if you have a mortgage, your mortgage servicer will typically require you to carry enough insurance to rebuild the home, according to the California Department of Insurance homeowners insurance guide.

If you own your home free and clear, you may not have a lender requiring homeowners insurance. But that does not mean going without insurance is a good idea for every homeowner.

For many people, a house is one of the largest assets they own. That makes insurance an important part of protecting that asset.

What Is a Home Warranty?

A home warranty, also called a home protection contract in California, is usually a service contract.

It may help pay to repair or replace certain covered home systems or appliances when they fail from normal wear and tear. The California Department of Insurance explains that home warranties are not the same as homeowners insurance and do not replace a homeowners policy.

In California, home warranty companies are regulated and licensed by the California Department of Insurance, so homeowners may want to check a company’s license status and complaint information before purchasing a contract.

Depending on the plan, a home warranty may include items such as:

- Heating systems

- Air conditioning, if included

- Plumbing systems

- Electrical systems

- Water heaters

- Ovens

- Dishwashers

- Built-in microwaves

- Washers and dryers, if included

- Garage door openers

Coverage varies widely.

One plan may include air conditioning. Another may charge extra for it. One plan may cover a built-in appliance but not a freestanding appliance. One plan may cover repair up to a certain dollar limit but not full replacement.

That is why the actual contract matters.

A home warranty is not a blank check for anything that breaks in the house.

Is a Home Warranty Required?

A home warranty is usually optional.

A buyer may choose to purchase one. A seller may offer one during a sale. Sometimes a home warranty is discussed as part of a real estate transaction.

In some cases, a home warranty may give a buyer more comfort during the first year of ownership.

But a home warranty does not replace homeowners insurance.

Home Warranty vs. Home Insurance: Quick Comparison

| Feature | Home Insurance | Home Warranty |

|---|---|---|

| Main purpose | May protect against covered sudden losses | May help with certain covered breakdowns |

| Common trigger | Fire, theft, wind, certain sudden water damage, liability issues | Normal wear and tear on covered systems or appliances |

| Required? | Usually required by mortgage lenders | Usually optional |

| Covers the home structure? | Often yes, subject to policy terms | Usually no |

| Covers appliances? | Usually not for simple breakdowns | Often yes, if listed and covered |

| Covers wear and tear? | Usually no | Often yes, if the item and issue are covered |

| Has deductibles or fees? | Usually yes | Usually service call fees and possible limits |

| Replaces the other? | No | No |

Real-Life Examples

The simple definition helps, but the examples are where the difference becomes clearer.

Example 1: The Dishwasher Stops Working

Let’s say your dishwasher suddenly stops cleaning properly. There is no major water damage. It is just not working anymore.

That is usually not the type of issue homeowners insurance is designed for.

If you have a home warranty and the dishwasher is covered, the warranty company may send a contractor to diagnose the issue. You may owe a service fee. Depending on the contract, the company may approve a repair or replacement.

But the details matter.

The contract may limit what parts are covered. It may exclude certain conditions. It may cap the amount the company will pay.

Example 2: A Pipe Breaks and Damages Flooring

Now let’s say a pipe suddenly breaks and water damages flooring, drywall, and personal belongings.

This is where things can get more complicated.

One problem may involve two different conversations:

- The failed system or part

- The damage caused by the failure

Homeowners insurance may help with resulting water damage if the event fits the policy terms.

A home warranty may help with the plumbing repair if that item and issue are covered under the warranty contract.

That is why homeowners should not assume one type of coverage handles everything.

Example 3: A Wildfire Damages the Home

If a wildfire damages or destroys a home, that is not a home warranty issue.

That is the type of major property loss where a homeowner would generally review the homeowners insurance policy.

A home warranty does not rebuild a home after a fire. It does not replace homeowners insurance. It is not designed to protect against major property losses like fire, natural disasters, or structural destruction.

For California homeowners, this is one of the most important distinctions to understand.

Example 4: The Air Conditioner Fails in Summer

If an air conditioning system stops working because of age or normal wear and tear, a home warranty may help if the system is covered.

But here is the part many homeowners miss:

Some home warranty plans charge extra for air conditioning coverage. Some have dollar limits. Some may exclude pre-existing conditions, improper installation, lack of maintenance, or certain parts. The Federal Trade Commission notes that home warranties often have limitations, fees, caps, and claims rules that homeowners should review carefully before buying.

Before buying a home warranty, ask:

- Is air conditioning included?

- What parts are excluded?

- Is there a dollar limit?

- Is there a service call fee?

- Can I choose my own contractor?

- What does the contract say about service timing?

- What happens if the item cannot be repaired?

- What maintenance records could be requested?

Those questions matter more than the brochure headline.

Why Homeowners Get Frustrated With Home Warranties

Home warranties can be helpful in the right situation, but they can also create frustration.

The frustration usually comes from expectations.

A homeowner may think, “I bought a warranty, so the repair should be covered.” The warranty company may say, “That part, condition, situation, or failure is excluded.”

This is why it is important to read the contract before buying.

Pay close attention to:

- Exclusions

- Service fees

- Coverage caps

- Waiting periods

- Cancellation rules

- Contractor rules

- Replacement limits

- Maintenance requirements

- Pre-existing condition language

- Items that cost extra to include

A long list of covered items may look impressive, but the exclusions and limits are where many claim decisions are made.

Why Homeowners Should Review Their Insurance Too

Many homeowners buy insurance once and then forget about it. That can be a mistake.

Your home changes over time.

Maybe you remodeled the kitchen. Maybe you upgraded the flooring. Maybe you added built-ins. Maybe construction costs have gone up. Maybe your roof is older now. Maybe your personal property has changed.

Your insurance should be reviewed from time to time so you understand whether it still fits your current home and your current risk.

A good insurance review may include:

- Dwelling coverage amount

- Replacement cost vs. actual cash value

- Roof coverage

- Deductibles

- Personal property limits

- Jewelry, art, collectibles, or other valuables

- Liability coverage

- Water damage limitations

- Earthquake coverage

- Flood coverage

- Wildfire-related requirements

- Additional living expense coverage

This is not the most exciting homeowner task. But it can matter a lot when something goes wrong.

The Big Mistake: Thinking One Replaces the Other

The biggest mistake is thinking home insurance and a home warranty do the same job.

They do not.

Home insurance is the protection homeowners usually rely on for covered major losses, property damage, personal property, and liability.

A home warranty is a service contract that may help with certain covered repairs or replacements of home systems and appliances.

One does not replace the other.

A warranty will not rebuild your home after a fire. Insurance usually will not replace an old dishwasher simply because it stopped working from normal use.

They solve different problems.

Should Sellers Offer a Home Warranty?

Some sellers may consider offering a home warranty. A seller-paid home warranty can be useful in certain home sales because it may give buyers more comfort during their first year of ownership.

That does not mean every seller needs to offer one.

It depends on the home, the buyer, the age of the systems, the local market, the offer strategy, and the overall negotiation.

A home warranty may be more attractive when:

- The home has older appliances

- The HVAC system is not brand new

- The buyer is nervous about repair costs

- The seller wants to create more buyer confidence

- The market is competitive and small incentives may help

But a warranty should not be used to hide known problems.

If a seller knows about an issue, the seller should discuss disclosure obligations with the appropriate real estate and legal professionals. A warranty is not a substitute for honesty, disclosure, or proper repairs.

Should Buyers Ask for a Home Warranty?

A buyer may want to consider asking for one, especially if they are buying an older home or moving from renting into ownership for the first time.

First-time homeowners often underestimate how many things they may be responsible for after closing:

- The water heater

- The garage door opener

- The dishwasher

- The garbage disposal

- The HVAC system

- The built-in microwave

A home warranty may help reduce some of that first-year uncertainty. But buyers should still read the plan, understand the service fees, and know what is not covered.

What This Means If You Are Thinking About Selling

This is where the topic becomes useful for sellers.

Buyers may not always ask about “home warranty vs. home insurance” in those exact words. But they often notice the clues:

- How old is the roof?

- How old is the HVAC system?

- Has the home been maintained?

- Are there signs of leaks?

- Will insurance be difficult?

- Will repairs be expensive after closing?

As a seller, you do not need to panic over every older item in the house. But you should understand how buyers may view the home.

In Irvine neighborhoods such as Turtle Rock, Woodbridge, Orchard Hills, Portola Springs, Turtle Ridge, and Great Park Neighborhoods, buyers often pay close attention to the age and condition of major home systems. They may notice the roof, HVAC, water heater, plumbing, appliances, garage systems, and signs of past leaks or maintenance.

A home does not need to be perfect before selling. But the more prepared a seller is, the easier it can be to answer buyer questions with confidence.

That may include gathering maintenance records, checking the age of major systems, reviewing roof condition, considering pre-listing repairs, and deciding whether a home warranty makes sense as part of the selling strategy.

This also connects to presentation.

When a home’s condition, maintenance, and major systems are easy to understand, it may help buyers feel more confident. Tony’s broader marketing approach considers preparation, professional presentation, buyer-focused content, custom home video, social media exposure, and clear communication as part of helping a listing make sense to buyers online and in person.

Smart Questions to Ask Before You Need Coverage

Before you buy or renew a home warranty, consider asking:

- What systems and appliances are covered?

- What is excluded?

- What is the service call fee?

- Is there a maximum payout per item?

- Can I choose the contractor?

- How fast does the company respond?

- What happens if the company denies the claim?

- Is the company licensed in California?

- What do customer complaints look like?

- Does this coverage duplicate something I already have?

Before you renew or change homeowners insurance, consider asking:

- Is my dwelling coverage enough for current rebuilding costs?

- What is my deductible?

- Do I have replacement cost coverage?

- What is excluded?

- Do I need earthquake or flood coverage?

- Are my valuables fully covered?

- Is my roof coverage limited?

- Do I have enough liability coverage?

- What happens if I need to live somewhere else during repairs?

- Has my policy kept up with improvements I made to the home?

Helpful Resources

For more information, you may want to review these resources:

- California Department of Insurance: Homeowners Insurance

- California Department of Insurance: Home Protection Contracts

- Federal Trade Commission: So what’s the deal with “home warranties”?

- National Association of Insurance Commissioners: My Insurance Doesn’t Cover What?

Final Thoughts

Home insurance and a home warranty are not the same thing.

Home insurance may help protect against covered losses involving the home, belongings, and liability. A home warranty may help with certain covered repairs or replacements when systems and appliances fail from normal wear and tear.

For homeowners, the best approach is simple:

Understand both before you need either one.

Read the policy. Read the warranty contract. Ask questions. Know the exclusions.

And when you are getting ready to sell, think about how the condition of your home, the age of your systems, and the confidence buyers feel can all affect your overall strategy.

FAQs About Home Warranty vs. Home Insurance

What is the main difference between a home warranty and home insurance?

Home insurance is generally for covered property losses, personal belongings, liability, and certain sudden damage events. A home warranty is usually a service contract that may help with certain covered repairs or replacements when home systems or appliances break down from normal wear and tear.

Does a home warranty replace homeowners insurance?

No. A home warranty does not replace homeowners insurance. A warranty may help with certain covered system or appliance breakdowns, while homeowners insurance may help with covered losses involving the home, belongings, and liability.

Is homeowners insurance required in California?

California does not generally require homeowners to carry homeowners insurance. However, if you have a mortgage, your mortgage servicer will typically require insurance coverage. Some properties may also have separate flood insurance requirements depending on location and lender rules.

Is a home warranty required when buying or selling a home?

A home warranty is usually optional. A buyer may purchase one, a seller may offer one, or it may become part of a negotiation, depending on the home, market, and contract terms.

Should Irvine sellers offer a home warranty?

Some Irvine sellers may consider offering a home warranty if the home has older systems or appliances and the warranty may help buyers feel more comfortable. Whether it makes sense depends on the home, buyer concerns, warranty terms, local market, and overall negotiation strategy.

What should homeowners read before buying a home warranty?

Homeowners should read the actual contract, especially the exclusions, service fees, coverage caps, contractor rules, replacement limits, maintenance requirements, and pre-existing condition language.

This article is for general educational information only and is not legal, insurance, tax, financial, warranty, claims, disclosure, or other professional advice. Coverage, obligations, rules, and outcomes depend on the specific policy, contract, property, facts, exclusions, limits, deductibles, service fees, professional guidance, and applicable laws. Always review your actual policy or contract and speak with your licensed insurance professional, warranty company, attorney, tax advisor, real estate professional, or other qualified professional before making decisions. If your property is currently listed or you are already represented by another real estate broker, this is not intended as a solicitation.

If you are thinking about selling a home in Irvine, Newport Beach, Newport Coast, South Orange County, or nearby coastal Orange County, I would be happy to help you look at your home through a buyer’s eyes and talk through what may be worth addressing before you go on the market.

Tony Babarino

California Real Estate Broker | REALTOR®

REAL Broker

Call/Text: (949) 633-6741

https://TonyBabarino.com

https://www.youtube.com/tonybabarino

https://www.instagram.com/tonybabarino

https://www.facebook.com/SOLDbyTonyBabarino/